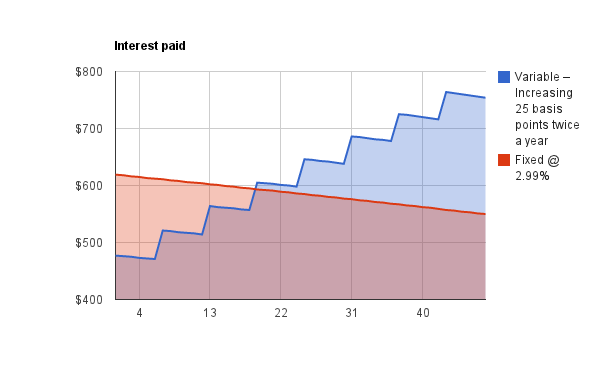

A home mortgage on which the rate of interest is set for the life of the loan is called a "fixed-rate home loan" or FRM, while a home loan on which the rate can change is an "adjustable rate home loan" or ARM. ARMs constantly have a fixed rate period at the beginning, which can range from 6 months to 10 years.

On any given day, Jones might pay a greater home loan rates of interest than Smith for any of the following factors: Jones paid a smaller origination charge, perhaps receiving an unfavorable charge or refund. Jones had a considerably lower credit rating. Jones is obtaining on a financial investment property, Smith on a primary residence.

Jones is taking "cash-out" of a re-finance, whereas Smith isn't. Jones requires a 60-day rate lock whereas Smith requires only one month. Jones waives the responsibility to keep an escrow account, Smith doesn't. Jones allows the loan officer to talk him into a higher rate, while Smith does not. All but the last item are genuine in the sense that if you shop on-line at a competitive multi-lender website, such as mine, the prices will vary in the method showed.

Rumored Buzz on Mortgages How Do They Work

Most brand-new home loans are offered in the secondary market quickly after being closed, and the prices charged debtors are always based upon existing secondary market value. The usual practice is to reset all prices every early morning based upon the closing costs in the secondary market the night prior to. Call these the lender's published costs.

This usually takes several weeks on a refinance, longer on a home purchase deal. To possible customers in shopping mode, a lending institution's posted cost has actually limited significance, considering that it is not offered to them and will vanish overnight. Published prices https://www.globenewswire.com/news-release/2020/06/10/2046392/0/en/WESLEY-FINANCIAL-GROUP-RESPONDS-TO-DIAMOND-RESORTS-LAWSUIT.html interacted to buyers orally by loan officers are especially suspect, due to the fact that a few of them downplay the rate to cause the buyer to return, a practice called "low-balling." The only safe way to go shopping posted prices is online at multi-lender website such as mine.

A (Lock A locked padlock) or https:// means you've securely linked to the.gov website. Share sensitive information only on authorities, safe websites.

Get This https://www.inhersight.com/companies/best/industry/financial-services Report about How Do Canadian Mortgages Work

A home mortgage loan or merely home mortgage () is a loan utilized either by purchasers of genuine property to raise funds to purchase genuine estate, or additionally by existing home owners to raise funds for any purpose while putting a lien on the home being mortgaged. The loan is "protected" on the borrower's residential or commercial property through a process referred to as mortgage origination.

The word home loan is originated from a Law French term used in Britain in the Middle Ages meaning "death pledge" and refers to the pledge ending (passing away) when either the obligation is satisfied or the residential or commercial property is taken through foreclosure. A mortgage can also be referred to as "a debtor offering factor to consider in the kind of a collateral for an advantage (loan)".

The lending institution will normally be a banks, such as a bank, cooperative credit union or building society, depending upon the nation worried, and the loan plans can be made either directly or indirectly through intermediaries. Features of mortgage such as the size of the loan, maturity of the loan, rate of interest, approach of settling the loan, and other qualities can vary significantly.

The 3-Minute Rule for How Mortgages Work In Monopoly

In many jurisdictions, it is normal for house purchases to be moneyed by a mortgage loan. Few individuals have adequate savings or liquid funds to enable them to buy residential or commercial property outright. In nations where the demand for house ownership is greatest, strong domestic markets for home mortgages have developed. Home mortgages can either be funded through the banking sector (that is, through short-term deposits) or through the capital markets through a process called "securitization", which converts swimming pools of home mortgages into fungible bonds that can be sold to financiers in little denominations.

For that reason, a home mortgage is an encumbrance (limitation) on the right to the property just as an easement would be, however because a lot of home mortgages happen as a condition for new loan cash, the word home mortgage has become the generic term for a loan secured by such real estate. Similar to other types of loans, home mortgages have an interest rate and are arranged to amortize over a set time period, normally thirty years.

Home loan loaning is the primary mechanism utilized in many countries to finance private ownership of domestic and commercial residential or commercial property (see industrial home mortgages). Although the terminology and exact types will vary from country to nation, the basic elements tend to be similar: Home: the physical house being financed. The exact type of ownership will vary from country to nation and might limit the types of lending that are possible.

The Ultimate Guide To How Do Mortgages Work

Constraints might consist of requirements to purchase house insurance coverage and home loan insurance coverage, or settle impressive debt before offering the residential or commercial property. Customer: the individual borrowing who either has or is developing an ownership interest in the residential or commercial property. Loan provider: any lender, however usually a bank or other monetary institution. (In some countries, particularly the United States, Lenders may also be financiers who own an interest in the home mortgage through a mortgage-backed security.

The payments from the debtor are afterwards gathered by a loan servicer.) Principal: the original size of the loan, which may or may not consist of certain other costs; as any principal is repaid, the principal will go down in size. Interest: a financial charge for usage of the loan provider's money (how do canadian mortgages work).

Conclusion: legal completion of the home mortgage deed, and hence the start of the home loan. Redemption: last repayment of the amount exceptional, which might be a "natural redemption" at the end of the scheduled term or a swelling sum redemption, normally when the customer decides to offer the property. A closed home loan account is stated to be "redeemed".

Not known Factual Statements About How Do Reverse Mortgages Work After Death

Governments normally manage numerous elements of home loan loaning, either straight (through legal requirements, for example) or indirectly (through guideline of the individuals or the monetary markets, such as the banking market), and typically through state intervention (direct loaning by the federal government, direct loaning by state-owned banks, or sponsorship of numerous entities).

Mortgage are usually structured as long-lasting loans, the regular payments for which resemble an annuity and determined according to the time value of cash solutions. The most basic arrangement would need a fixed month-to-month payment over a duration of 10 to thirty years, depending upon regional conditions.

In practice, numerous versions are possible and typical worldwide and within each country. Lenders offer funds against residential or commercial property to earn interest income, and usually obtain these funds themselves (for instance, by taking deposits or providing bonds). The cost at which the loan providers obtain cash, therefore, affects the expense of borrowing.

The Of How Does Mortgages Work Reddit

Home loan loaning will likewise take into consideration the (perceived) riskiness of the home loan, that is, the possibility that the funds will be repaid (normally thought about a function of the creditworthiness of the debtor); that if they are not paid back, the lending institution will have the ability to foreclose on the realty assets; and the financial, rate of interest danger and dead time that might be involved in certain circumstances.